Sassetti LLC

The Most Overlooked Single Audit Requirement: Suspension & Debarment (and Why Documentation Is Everything)

The most overlooked Single Audit requirement is often not about allowability, procurement thresholds, or reporting deadlines. It is something much simpler and completely avoidable: nonprofits forget to document their Suspension and Debarment checks.

Under 2 CFR §200.214, every recipient and subrecipient of federal funds must follow the federal government’s suspension and debarment rules, which are implemented through 2 CFR Part 180. The regulation states that recipients and subrecipients are subject to the nonprocurement debarment and suspension regulations, as well as 2 CFR Part 180.

Part 180 explains what organizations must do before entering into covered transactions, which generally are federal grant funded contracts and subawards that your procurement policy subjects to suspension and debarment checks. In practice, this usually means contracts for goods or services and subawards under federal awards above your micro‑purchase threshold (the level at or below which micro‑purchase procedures apply) or other internal threshold, where your procedures require verifying that the other party is not suspended, debarred, or otherwise excluded. Your procurement policy should clearly define which contracts and subawards are covered transactions (for example, all subawards and all contracts over a predetermined federal awards).

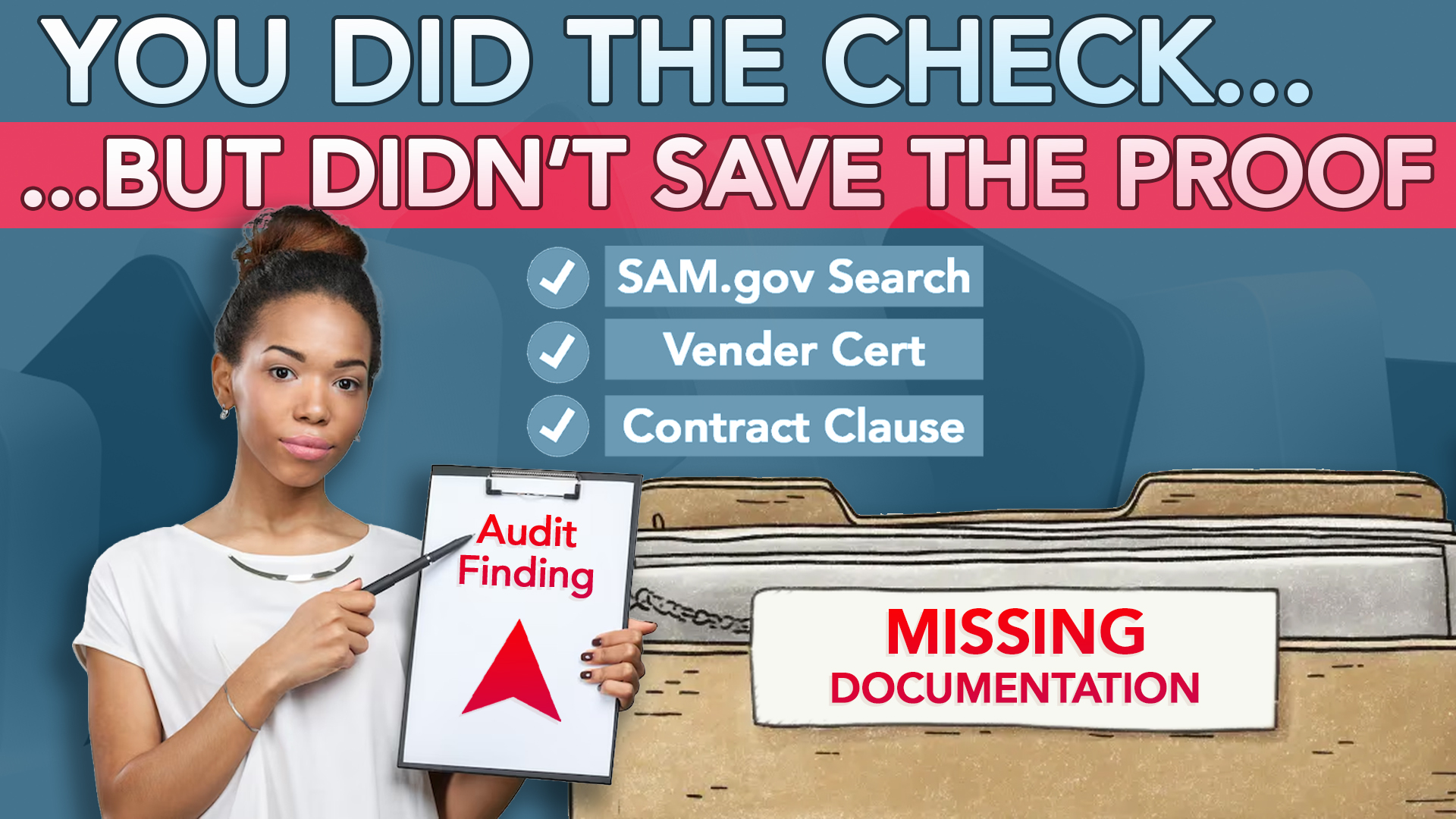

The three acceptable ways to verify a vendor

Under 2 CFR §180.300, you can verify that a vendor is not debarred or suspended using any one of the following methods:

- Check SAM.gov exclusions

- Obtain a signed vendor certification

- Include a suspension and debarment clause in the contract

That is all that is required. You do not need a complex system or checklist. You only need to use one of these three methods, and you must document it.

Why this becomes a finding

Most nonprofits actually perform the check. The problem appears at audit time, when there is no:

- Screenshot or PDF of the SAM.gov search

- Signed certification saved to the file

- Executed contract showing the suspension and debarment clause

From an audit perspective, if there is no support, it did not happen.

The 2025 OMB Compliance Supplement continues to emphasize Procurement and Suspension and Debarment as a core compliance area, especially with the split Part 3 sections (Part 3.1 and Part 3.2) depending on whether an award falls under the pre‑2024 or revised 2024 Uniform Guidance. Nonprofits need clear, consistent evidence in every procurement file, especially during this transition period.

How long to keep the documentation

Uniform Guidance retention rules require nonprofits to keep all federal award documentation, including suspension and debarment support, for three years after the final financial report is submitted (2 CFR §200.334). Organizations must keep records longer if litigation, audit issues, or claims are unresolved.

A simple, audit‑ready suspension and debarment process

Here is an easy workflow every organization can use, and should include as part of its procurement policy:

Conclusion

- Before approving a vendor, complete one of the three verification methods previously listed.

- Save the proof, such as a PDF, screenshot, signed form, or contract.

- File it with the invoice, purchase order, or contract.

- Recheck annually for multiyear contracts (recommended).

- Retain the documentation for the required period.

This process takes less than two minutes and can eliminate a finding that appears year after year for many nonprofits.

Final thought

Suspension and debarment compliance is not complicated or highly technical, and it is usually not high risk. It is, however, a clear example of how small documentation gaps can lead to unnecessary Single Audit findings. A simple saved PDF or email can prevent avoidable findings, reduce stress, and limit the need for corrective action plan.

Author: Aroosa Shahab

Footer

Sassetti LLC © 1921-

2026